- News

- Business News

- India Business News

- Falling FD rates set to hit 4 crore senior citizens hard

Trending

This story is from October 10, 2019

Falling FD rates set to hit 4 crore senior citizens hard

On Wednesday, along with a cut in lending rates, banking major SBI also cut the FD rates for senior citizens for 1-2 years bracket to 6.9% from 7% while savings bank rate was cut to 3.25% from 3.5% for deposits of up to Rs 1 lakh. Other banks are expected to follow. Financial planners say senior citizens will have to take some risks and invest in debt funds.

Many senior citizens are dependent on deposits and savings in banks

Key Highlights

- On Wednesday, SBI cut the FD rates for senior citizens for 1-2 years bracket to 6.9% from 7%

- Move to sub-6% FD rates looks inevitable, experts say

- Financial planners say, senior citizens will have to take some risks and invest in marked-to-market products like debt funds

MUMBAI: Senior citizens and retirees who primarily depend on income from fixed deposits in banks, may soon need to look at shifting part of their life's savings into debt mutual funds.

On Wednesday, along with a cut in lending rates, banking major SBI also cut the FD rates for senior citizens for 1-2 years bracket to 6.9% from 7% while savings bank rate was cut to 3.25% from 3.5% for deposits of up to Rs 1 lakh.Other banks are expected to follow.

Thanks to the Reserve Bank of India (RBI), banks have moved to an external benchmark-the repo rate that is variable-to fix interest rates for their borrowers. With the lending rate being marked to a variable rate, now it's almost a given that the rate of interest on deposits will also be linked to the same variable benchmark.

In a falling interest rate scenario, when the RBI cuts repo rate to spur growth, FD rates are bound to fall, hurting those senior citizens and retirees dependent on FD income to meet their financial needs.

Alternately, the government has to step in to help senior citizens through tax concessions on the senior citizen savings scheme (SCSS) in which up to Rs 15 lakh could be parked by each individual of above 60 years, a report by SBI said.

Post SBI's cut, yield on an FD of Rs 50 lakh translates to a reduction in yearly income by Rs 5,000. SBI said that the rates have been cut 'given the surplus liquidity in the system'.

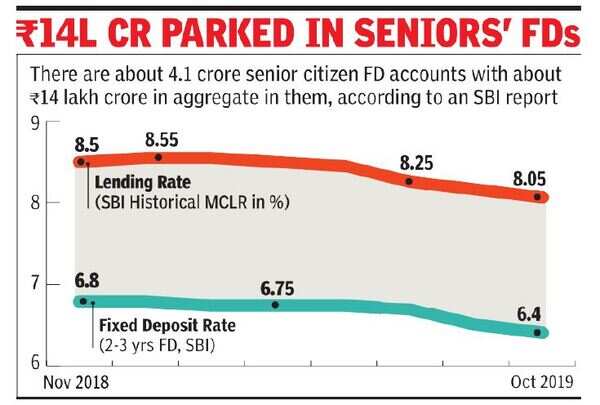

According to an SBI report, it is estimated that currently there are about 4.1 crore senior citizen FD accounts with about Rs 14 lakh crore in aggregate parked in them. All this money could be hit when these FDs are renewed at a lower rate and lead to resentment among depositors.

Earlier, speaking to TOI, PNB chief S S Mallikarjuna Rao had said that there is a limit below which rates can't be reduced. Repo rate has come down to the lowest level in the last nine-ten years and there is an indication it may reduce further. "In our country, if deposits go below 6%, there will be social uneasiness as many senior citizens depend on the interest income," he warned.

Speaking to TOI, Rajkiran Rai, MD, Union Bank of India, said: "Historically, inflation has been high at over 5%, which is why people are accustomed to 8% on fixed deposits. Now inflation is below 4% and deposit rates are in the range of 6-7% which means that real interest rates have not moved much," he said. He added that the feeling of discomfort is because people are not accustomed to low rates. "The other angle is that if the economy does not grow, everyone will be at a disadvantage," he said.

The move to sub-6% FD rates, however, looks inevitable. "Eventually, banks will have to move to a floating rate regime but in the short term the move will face a lot of resistance from depositors as they are not used to floating rate deposits," said Gajendra Kothari, MD & CEO, Etica Wealth Management.

According to Kothari, senior citizens should park Rs 15 lakh in SCSS and the balance in the government's 7.75% deposit schemes. However, both are currently taxable. In case the government does not give any tax sops to these schemes and FD rates are reduced farther, higher rated debt mutual funds, which offer about 7.5%-8% return, could turn out to be attractive investment avenues for senior citizens in the higher tax bracket. "A lot of money will start flowing to debt MFs as they have already been offering a higher floating rate return and with better diversification," Kothari said. "And if one is willing to park money for more than three years, the tax implications after indexation benefits will be very less."

When it comes to the need to maintain the same lifestyle while income from FDs is falling, investors could look at highly rated corporate FDs which are at least as good as the banks where the FDs were, said Surya Bhatia, managing partner, Asset Managers, a Delhi-based financial advisory outfit. The other alternative is to look at debt MFs that provide high safety with long-term capital gains (LTCG) benefits and have rundown maturity that lowers risks.

According to Bhatia, while looking for higher returns from new assets to match the reduced income from FDs, senior citizens should not compromise on three important aspects: Safety, return and liquidity. "Fit in where you can but don't compromise on any of the aspects," Bhatia said. "Don't chase return by compromising on the other two aspects."

On Wednesday, along with a cut in lending rates, banking major SBI also cut the FD rates for senior citizens for 1-2 years bracket to 6.9% from 7% while savings bank rate was cut to 3.25% from 3.5% for deposits of up to Rs 1 lakh.Other banks are expected to follow.

Thanks to the Reserve Bank of India (RBI), banks have moved to an external benchmark-the repo rate that is variable-to fix interest rates for their borrowers. With the lending rate being marked to a variable rate, now it's almost a given that the rate of interest on deposits will also be linked to the same variable benchmark.

In a falling interest rate scenario, when the RBI cuts repo rate to spur growth, FD rates are bound to fall, hurting those senior citizens and retirees dependent on FD income to meet their financial needs.

In such a scenario, say financial planners, senior citizens will have to take some risks and invest in marked-to-market products like debt funds.

Alternately, the government has to step in to help senior citizens through tax concessions on the senior citizen savings scheme (SCSS) in which up to Rs 15 lakh could be parked by each individual of above 60 years, a report by SBI said.

Post SBI's cut, yield on an FD of Rs 50 lakh translates to a reduction in yearly income by Rs 5,000. SBI said that the rates have been cut 'given the surplus liquidity in the system'.

According to an SBI report, it is estimated that currently there are about 4.1 crore senior citizen FD accounts with about Rs 14 lakh crore in aggregate parked in them. All this money could be hit when these FDs are renewed at a lower rate and lead to resentment among depositors.

Earlier, speaking to TOI, PNB chief S S Mallikarjuna Rao had said that there is a limit below which rates can't be reduced. Repo rate has come down to the lowest level in the last nine-ten years and there is an indication it may reduce further. "In our country, if deposits go below 6%, there will be social uneasiness as many senior citizens depend on the interest income," he warned.

Speaking to TOI, Rajkiran Rai, MD, Union Bank of India, said: "Historically, inflation has been high at over 5%, which is why people are accustomed to 8% on fixed deposits. Now inflation is below 4% and deposit rates are in the range of 6-7% which means that real interest rates have not moved much," he said. He added that the feeling of discomfort is because people are not accustomed to low rates. "The other angle is that if the economy does not grow, everyone will be at a disadvantage," he said.

The move to sub-6% FD rates, however, looks inevitable. "Eventually, banks will have to move to a floating rate regime but in the short term the move will face a lot of resistance from depositors as they are not used to floating rate deposits," said Gajendra Kothari, MD & CEO, Etica Wealth Management.

According to Kothari, senior citizens should park Rs 15 lakh in SCSS and the balance in the government's 7.75% deposit schemes. However, both are currently taxable. In case the government does not give any tax sops to these schemes and FD rates are reduced farther, higher rated debt mutual funds, which offer about 7.5%-8% return, could turn out to be attractive investment avenues for senior citizens in the higher tax bracket. "A lot of money will start flowing to debt MFs as they have already been offering a higher floating rate return and with better diversification," Kothari said. "And if one is willing to park money for more than three years, the tax implications after indexation benefits will be very less."

When it comes to the need to maintain the same lifestyle while income from FDs is falling, investors could look at highly rated corporate FDs which are at least as good as the banks where the FDs were, said Surya Bhatia, managing partner, Asset Managers, a Delhi-based financial advisory outfit. The other alternative is to look at debt MFs that provide high safety with long-term capital gains (LTCG) benefits and have rundown maturity that lowers risks.

According to Bhatia, while looking for higher returns from new assets to match the reduced income from FDs, senior citizens should not compromise on three important aspects: Safety, return and liquidity. "Fit in where you can but don't compromise on any of the aspects," Bhatia said. "Don't chase return by compromising on the other two aspects."

About the Author

Partha SinhaEnd of Article

FOLLOW US ON SOCIAL MEDIA

Hot Picks

TOP TRENDING

Trending Stories

In Business

Entire Website

- Will banks open only for 5 days a week? Here’s what you should know about IBA’s proposal

- India set to be third largest economy, says S&P Global

- Dalal Street bull run continues! BSE Sensex crosses 69,000 for the first time; Nifty above 20,800

- Byju’s reduces notice period for employees as troubles mount

- Sensex surges over 900 points, Nifty above 20,550 as BJP state election wins bolster Modi's Lok Sabha 2024 prospects

- UltraTech to buy building materials business of Kesoram in 7,600 crore deal

- Tata Technologies stock debuts at a bumper 140% premium; share price at Rs 1200 on BSE

- Tata Technologies share allotment: How to check IPO allotment status, listing date, GMP

- BSE m-cap rides rally in Adani stocks, tops $4 trillion

- Charlie Munger, who helped Warren Buffett build Berkshire, dies at 99

- Son gave supari to kill parents, bro; hitmen killed 3 guests instead in Karnataka's Gadag

- Patanjali: SC poses tough questions to IMA, seeks govt response

- What’s the best way to treat irritable bowel syndrome?

- Buzz on after cleaning, renovation work begin at Rahul's Amethi house

- 'New Putin in making': Sharad Pawar attacks PM Modi

- Congress Surat pick Kumbhani 'missing', likely to join BJP

- How you can gain by planting trees under Green Credit plan

- Jio MD Mashruwala resigns: Read the company's stock exchange filing

- Court extends judicial custody of Kejriwal, K Kavitha till May 7

- Hesson reveals reason behind Chahal's departure from RCB

Popular Categories

Hot on the Web

Top Trends

MP Board Class 5 ResultRohit SharmaIPL Today MatchStock Market TodayCUET UG Date SheetIsrael Iran WarJEE Main Session 2 ResultArvind KejriwalMalaysian Navy Helicopter CrashIPL Live ScoreIPL Orange Cap 2024IPL Purple Cap 2024IPL 2024 ScheduleLok Sabha Election Full ScheduleIPL Points TableIPL Match Full Schedule

Trending Topics

Hanuman Jayanti WishesMargot RobbieOptical IllusionRanveer SinghAishwarya RaiRajkumar RaoPink Full Moon 2024Sharmila TagoreRavi KishanPink MoonMunawar FaruquShilpa ShettyAmitabh BachchanChiranjeeviRupali GanulyKalki 2898 ADBest Bluetooth SpeakersBest Laptop Under30000Best 75 Inch Smart TvBest 24 Inch Tv

Living and entertainment

Latest News

At least five migrants die in attempt to cross English Channel, French police saysWhile the strong wave of uncertainty hits, these 5 top meme coins show a certain positive trendDelhi excise policy case: Arvind Kejriwal, K Kavitha's judicial custody extended till May 7Emily Blunt and Ryan Gosling's action-comedy 'The Fall Guy' to release in India on May 3!Constable shoots self after wife hangs herself in UP's ChitrakootOnly Self-Transformation Can Lead To Ram RajyaZerodha’s Nikhil Kamath buys big part of Sachin Bansal’s holding in Ather Energy; says ‘among the largest bets’Facing pressure from rights groups, World Bank suspends funding for Tanzania tourism projectUS commander: China is fast becoming more aggressive in regionIrfan Pathan says watch out for these three Indian players at T20 World CupSalman Khan house firing: Mumbai crime branch recovers second pistol from Tapi river in SuratWatch: MS Dhoni flaunts muscle-power with Thala-esque sixes ahead of CSK vs LSG matchCongress Surat candidate Nilesh Kumbhani 'missing', likely to join BJP; party workers stage protestAt 22%, lake water stock hits 3-yr low; no cut yet, says BMCLok Sabha elections 2024 full schedule: Ajmer to vote on April 26IPL 2024 Purple Cap Update: MI's Jasprit Bumrah 1st, RR's Yuzvendra Chahal 2nd and PBKS' Harshal Patel 3rd after match 38WhatsApp to soon roll out channel update forwarding feature: Here’s what it means for usersThese countries have banned the sale of MDH and Everest masalas

Copyright © 2024 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service